Diving into the World of ITC Share Price Hey there, if you’re tuning into the Indian stock market, you’ve probably heard the buzz around ITC Limited lately. As someone who’s followed conglomerates like this for years, I can tell you ITC isn’t just another stock—it’s a powerhouse with fingers in everything from cigarettes to hotels and snacks. But right now, as we kick off 2026, its share price is making headlines for all the dramatic reasons.

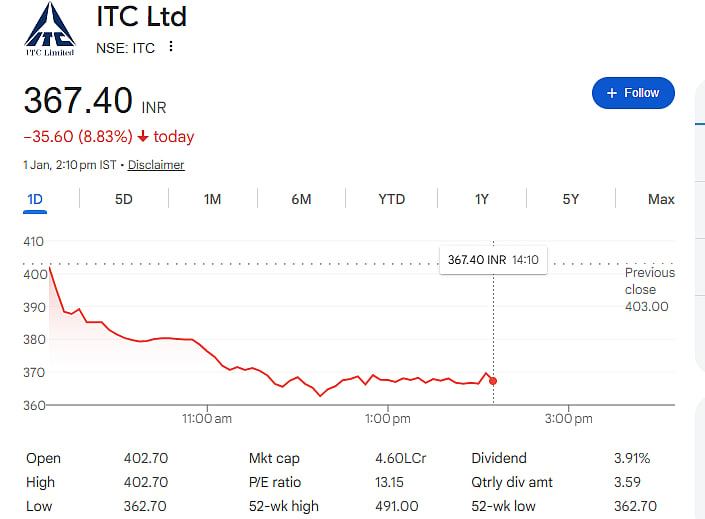

On January 1, 2026, ITC closed at ₹363.95 on the NSE, marking a sharp 9.69% drop from the previous close of ₹403. That’s a whopping ₹50,000 crore wipe out in market cap in a single day! If you’re wondering why this happened and what it means for investors, let’s break it down step by step. I’ll keep it straightforward, like we’re chatting over coffee, but with solid facts and insights to back it up. Diving into the World of ITC Share Price

Diving into the World of ITC Share Price First off, a quick intro to ITC for anyone new to the game. Founded way back in 1910 as Imperial Tobacco Company of India, ITC has evolved into a diversified giant. Its headquarters in Kolkata isn’t just an office—it’s a symbol of its green initiatives, like the LEED-certified ITC Green Centre. Diving into the World of ITC Share Price

Today, the company dominates in tobacco (think Gold Flake and Wills cigarettes), fast-moving consumer goods (FMCG) like Aashirvaad atta and Sunfeast biscuits, hotels (ITC Hotels chain), paperboards, and even agri-business. It’s a staple in many Indian portfolios because of its stability and dividends. But as we’ll see, that tobacco arm—contributing about 80% of profits—can be a double-edged sword.

A Look Back: ITC’s Share Price Journey

Diving into the World of ITC Share Price To understand where ITC’s share price stands today, we need to rewind a bit. Over the past five years, the stock has been a solid performer, delivering around 105% returns. That’s not bad for a company in mature industries. Back in 2020, during the pandemic dip, shares were trading as low as ₹160, offering a juicy 6% dividend yield that screamed “value buy.” Fast forward to early 2025, and it hit a 52-week high of ₹491, buoyed by strong FMCG growth and the demerger of its hotels business, which unlocked some value for shareholders.

But 2025 wasn’t all smooth sailing. The stock dipped to a 52-week low of ₹390.15 before the recent plunge pushed it even lower to ₹362.70 intraday on January 1, 2026. Year-to-date in 2026 (okay, it’s only day two, but based on 2025 trends), it’s down about 12%, underperforming the broader market. Why the rollercoaster? Well, ITC’s performance has historically been tied to economic cycles, consumer spending, and regulatory shifts. For instance, during the 2016 demonetization, shares took a hit as cash-dependent rural markets slowed. But it bounced back strong, thanks to its diversified portfolio.

Diving into the World of ITC Share Price

Let’s throw in some numbers for context. In the last three years, ITC’s return on equity (ROE) has averaged a healthy 28%, and it’s almost debt-free. Trading volume on January 1 was massive—over 11.8 million shares on BSE alone, with a market cap hovering around ₹5.03 lakh crore. If you’re a visual person, here’s a recent stock chart showing that steep drop—notice how it hit the lower circuit amid the panic.Diving into the World of ITC Share Price

ITC Shares Crash Over 10%, Lower Circuit Hits Stock, Excise Duty …

What Drives ITC’s Share Price? Breaking Down the Key Factors

Diving into the World of ITC Share Price Now, onto the meaty part: what really moves ITC’s needle? As an expert in this space, I’ve seen how a mix of internal strengths and external pressures shape its valuation. Let’s unpack it.

Diving into the World of ITC Share Price

- The Tobacco Dominance and Regulatory Risks: Cigarettes are ITC’s cash cow, but they’re also its Achilles’ heel. The recent 10% plunge? Blame it on the government’s new excise duty on cigarettes, effective February 1, 2026. This isn’t just a tweak—it’s a levy per 1,000 sticks (ranging from ₹2,050 to ₹8,500 based on length), on top of the existing 40% GST. For longer cigarettes (over 75mm, about 16% of ITC’s volumes), prices could jump ₹2-3 per stick. Analysts like Jefferies warn this could dent volumes by 5% in FY27, squeezing margins if ITC absorbs some costs.Take a real-world example: Back in 2017, when GST rolled out, cigarette prices spiked, and illegal smuggling surged. History might repeat, with premium brands hit hardest. On X (formerly Twitter), investors are buzzing— one post noted how this tax could boost black-market sales, hurting legal players like ITC.

- Diving into the World of ITC Share Price

- Diversification Efforts and Market Trends: ITC isn’t all smokes. Its FMCG segment (products like Yippee noodles and Engage perfumes) has grown steadily, with brands that resonate in everyday Indian life.

ITC Group: History, Milestones, and Shareholding Structure

But despite two decades of pushing non-tobacco businesses, they still only chip in about 20% of profits. The 2025 hotels demerger was a win, but uncertainties around valuation added pressure. Broader factors like inflation, rural demand, and competition from players like Hindustan Unilever also play in. Diving into the World of ITC Share Price

- Economic and Investor Sentiment: ITC trades at a PE of around 25-30, higher than global tobacco peers (low teens) due to its Indian growth story. But with BAT (British American Tobacco) potentially selling more stakes, supply could flood the market. Plus, block deals like the 4 crore shares traded at ₹400 on Jan 1 added to the volatility.

A case study? Compare ITC to Godfrey Phillips, another tobacco player. Godfrey’s shares tanked 19% on the same news, but it’s up 250% over three years—pure tobacco focus made it riskier but rewarding. ITC’s diversification cushions blows, but doesn’t eliminate them.

Diving into the World of ITC Share Price

Future Outlook: Opportunities Amid the Smoke?

Peering ahead, experts are mixed but cautious. Wall Street targets average ₹504, with highs up to ₹595, suggesting 30-40% upside from current levels. Earnings growth is pegged at 10.2% annually, with revenue up 6.5%. Q2 2025-26 profits rose 2.67% to ₹5,126 crore, showing resilience.

But brokerages like Nuvama downgraded to ‘Hold,’ citing 20%+ price hikes and potential EBITDA cuts. Motilal Oswal and others slashed targets too. Intrinsic value estimates put it at ₹269, hinting at overvaluation. On the flip side, if prices fall further, dividend yield could hit FD levels (currently 3.94%). One X user calculated: ₹1 lakh at ₹360 yields about 3.99% from ₹14.35 dividends.

Expert take? Muthukrishnan Dhandapani, a seasoned investor, calls it a potential value trap unless non-tobacco profits surge. Regulatory uncertainty looms, but ITC’s cash flows and brands could shine if it navigates the tax storm.

Wrapping It Up: Is ITC Worth Your Bet?

In the end, ITC’s share price story is a classic tale of resilience meets risk. It’s not flashy like tech stocks, but its dividends and diversification make it a defensive play for long-term holders. If you’re in it for stability, the current dip might be a buying window—especially if volumes hold post-February. But if tobacco taxes keep rising, expect more bumps. As always, do your homework; markets are unpredictable, but informed decisions win the day. What do you think—holding, buying, or sitting it out? Drop your thoughts Diving into the World of ITC Share Price